.png@webp)

.png@webp)

Published Sep 13, 2021

Online travel agents (OTAs) operate on thin profit margins and must optimise their operations to protect and grow their businesses. One way is through payments, as inefficient payments systems can be costly and jeopardise customer experience – both of which will damage the bottom line.

Below are five payment challenges for OTAs and how they can make payment processing more efficient.

1. Risk of payments fraud

An inefficient payment systems are vulnerable to fraud. Not only will fraud have an immediate effect on profit margins, it will also dent a business’s reputation and can have a big impact on retaining and attracting customers. According to IBM, travel and transportation is the second most targeted industry for cybercriminals. As intermediaries, OTAs are particularly vulnerable and their reputations are easily tarnished by OTA scams, as underlined by Ryanair in 2021.

With the growth of card-not-present transactions, fraud is always a major concern when paying suppliers and receiving payments. Hence, OTAs must choose payment partners who offer secure platforms and a range of secure payment methods. As a minimum, OTAs must ensure that their payment providers offer end-to-end encryption and PCI DSS compliant credit card processing.

In terms of comparative fraud rates, credit and debit cards are riskier than bank transfers and airline settlement plans, while virtual cards [link to previous virtual cards blog] offer the best protection.

2. Costly cross-border payments

Travel is an international business and globalisation means that companies of all types are increasingly trading across borders. OTAs have suppliers and customers spread worldwide, and need reliable and cost-efficient cross-border payments for international trade. But there are many costs and risks, such as fluctuating foreign exchange rates, transaction fees, the constant threat of fraud, long settlement times, regulatory requirements, and geopolitical uncertainty.

OTAs must offer a wide range of payment methods and handle multiple currencies, backed by strong fraud and risk management. Bank transfers and plastic cards have higher transaction costs, while airline settlement plans and virtual cards are cost-efficient alternatives.

Digitalisation is advancing rapidly and improving cross-border payments. Virtual and mobile payments are key trends, and virtual cards are well suited to cross-border payments because of their versatility, low risk and ease of integration via APIs. According to Juniper Research, the global transaction value of virtual cards will reach $6.8 trillion in 2026.

3. Complex reconciliations

Cross-border payments are far from straightforward. Today there are numerous payment providers and payment methods to choose between, and chargebacks and reversals mean it can be time-consuming and costly to process transactions. When errors creep in, they compound the problem, and if there is poor transparency and weak control, it can be easy to miss fraudulent transactions. This is where virtual cards excel, as they eliminate manual processing and fraud, and make reconciliation easy.

4. Difficult transaction dispute/reimbursement process

Payment disputes are a fact of life for any business, and disputed online transactions and consequent chargebacks are particularly prevalent. If you make payments by bank transfer, there is little or no comeback. Once the money has left an account it’s usually gone for good. With airline settlement plans, the dispute and refund process is heavily weighted in favour of airlines. With card payments, chargebacks offer a trusted dispute process, and with virtual cards there is the added benefit of stronger fraud protection.

5. Poor liquidity

Stable cash flow is vital for all businesses, particularly travel sector players. With tight profit margins, liquidity makes the difference between a business thriving or not. Unsurprisingly, Covid-19 has underlined the importance of cash reserves and positive cash flow.

OTAs need to maximise the time funds are held in their accounts, which depends on their payments strategy. Cards are a good option because they extend the number of days agents can keep customers’ money until they settle with the card company. Best of all are virtual cards, because they preserve liquidity. You can customise the transaction date so that money stays in your account as long as possible between payment by your customer and when funds are forwarded to the merchant/supplier.

How Nium boosts payment efficiency

As a global platform providing cross-border and omnichannel payments, we can increase the efficiency of payments for any online travel agent. Nium can reduce payment fees and improve the convenience, transparency and speed of payments wherever you operate. We do this by:

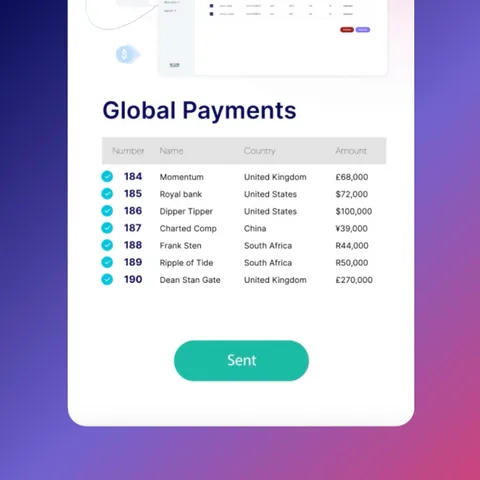

- Reducing transaction and foreign exchange fees for international payments.

- Accelerating the collection of money locally; converting it to the desired currency and executing bank transfers in real-time; and making real-time, same-day payments globally.

- Facilitating global expansion by managing payment requirements in new countries and regions as your business grows.

To find out more, see our travel page or contact us to discuss what Nium can do for your business.